Financial advisors’ productivity is becoming ever more important as a performance metric as a result of intensifying competition and increasing client segmentation.

As such, Investment Executive‘s (IE) analysis of data gathered during this year’s Report Card series highlights the overall dominance of the large financial services institutions — including banks and life insurance giants — within the retail investment business in terms of relative productivity. At the same time, the analysis also reveals that productivity isn’t everything as the industry’s best-paid sales forces aren’t necessarily also the most productive.

The seven charts included in this slideshow detail the relative productivity of each firm surveyed in this year’s Report Card series. To calculate relative productivity, IE compares the average assets under management (AUM) per client for each firm with the average for that specific distribution channel. This means brokerages would be compared with brokerages, mutual fund and full-service dealers would be compared with fellow dealers, banks with banks, and insurance agencies with other insurance agencies.

Firms that appear above the 0% mark on the y-axis are more productive than average in their distribution channel while firms that fall below 0% on the y-axis have productivity that is below average. A firm that appears right around the 0% figure is more or less in line with its channel’s average productivity.

So, for example, if a brokerage firm has a relative productivity score of 20%, this means the firm is 20% more productive than the average for the brokerage channel. Similarly, an insurance agency with a relative productivity of -10% would be below the average by 10% compared with other firms in that channel.

Gauging advisors’ relative productivity

Gauging advisors’ relative productivity

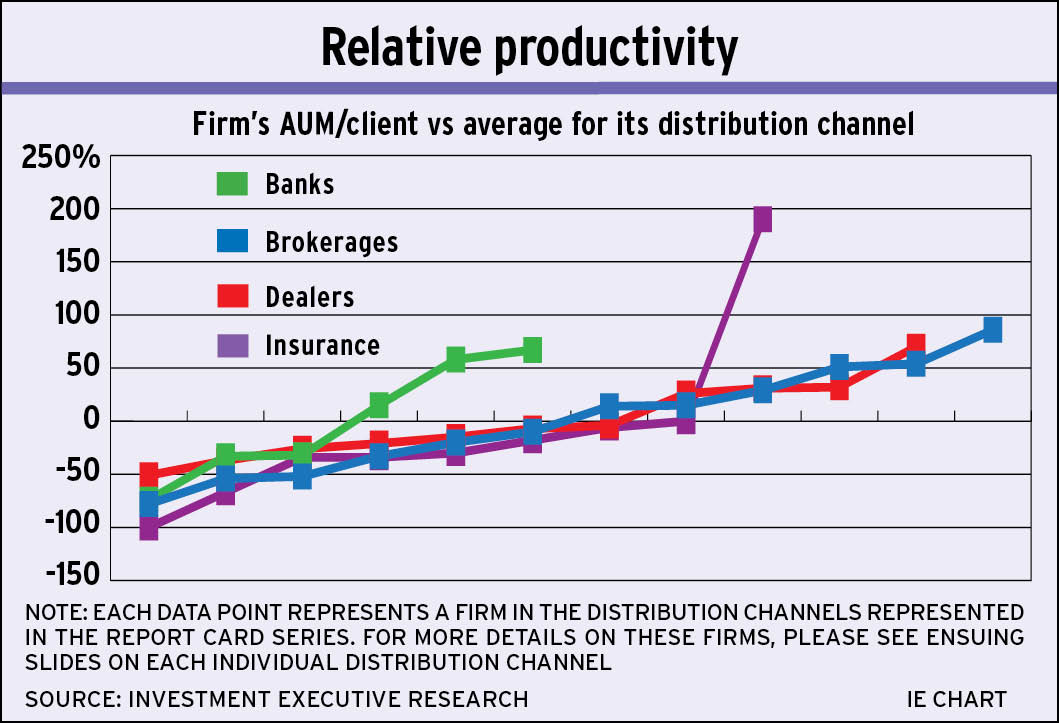

Relative Productivity

This chart highlights how the various distribution channels in the financial services sector fare. For example, both brokerages and dealers have very similar distribution patterns. The insurance channel appears to follow a similar pattern, with the exception of one major outlier — PPI Advisory — that stands far above the rest of the firms in that segment, leaving most of the others below the average. The data on the banks shows a wider disparity between the top performers and the rest of the channel, although this is largely attributable to the smaller number of firms in this channel.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive

Gauging advisors’ relative productivity

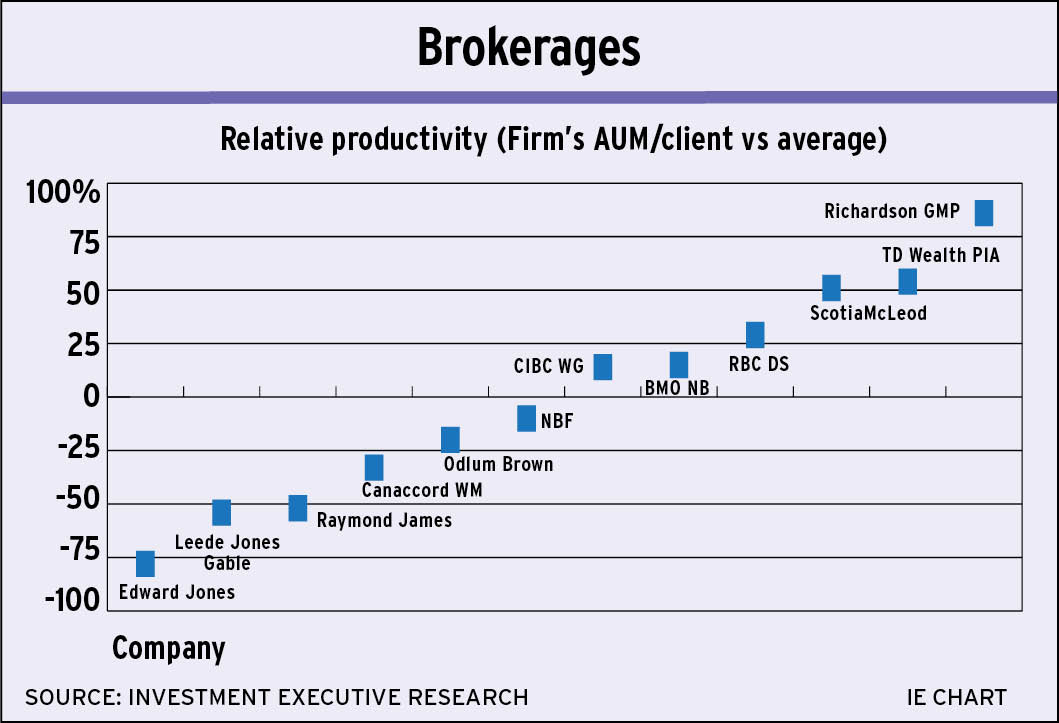

Brokerages

This chart reveals that the bank-owned firms dominate the brokerage channel in terms of relative productivity. The investment dealer subsidiaries of the Big Five banks all have above-average rankings. Nevertheless, it’s an independent firm, Toronto-based Richardson GMP Ltd., that leads the brokerages as advisors with the firm report an AUM/client metric that’s almost double the industry average. That said, the rest of the industry’s independents are trailing the big bank-owned dealers.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive

Gauging advisors’ relative productivity

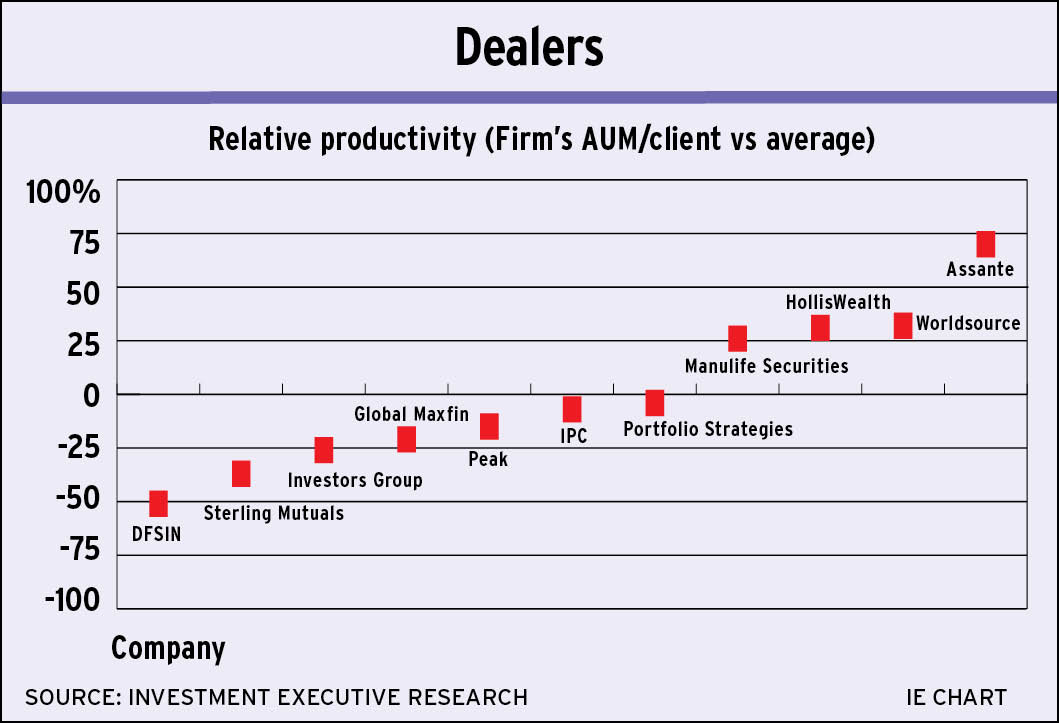

Dealers

Toronto-based Assante Wealth Management (Canada) Ltd. is the clear leader in the dealer channel in terms of relative productivity. The firm is easily outpacing most of its peers, with average relative AUM/client that’s almost double the overall average in this channel. Despite being well back of Assante, the other outperformers in the dealer space — Manulife Securities, HollisWealth Inc. and Worldsource Wealth Management Inc. — are also handily above average as their advisors’ average AUM/client is more than 20% above the average. The firms lagging in terms of relative productivity are, for the most part, not that far off the overall average.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive

Gauging advisors’ relative productivity

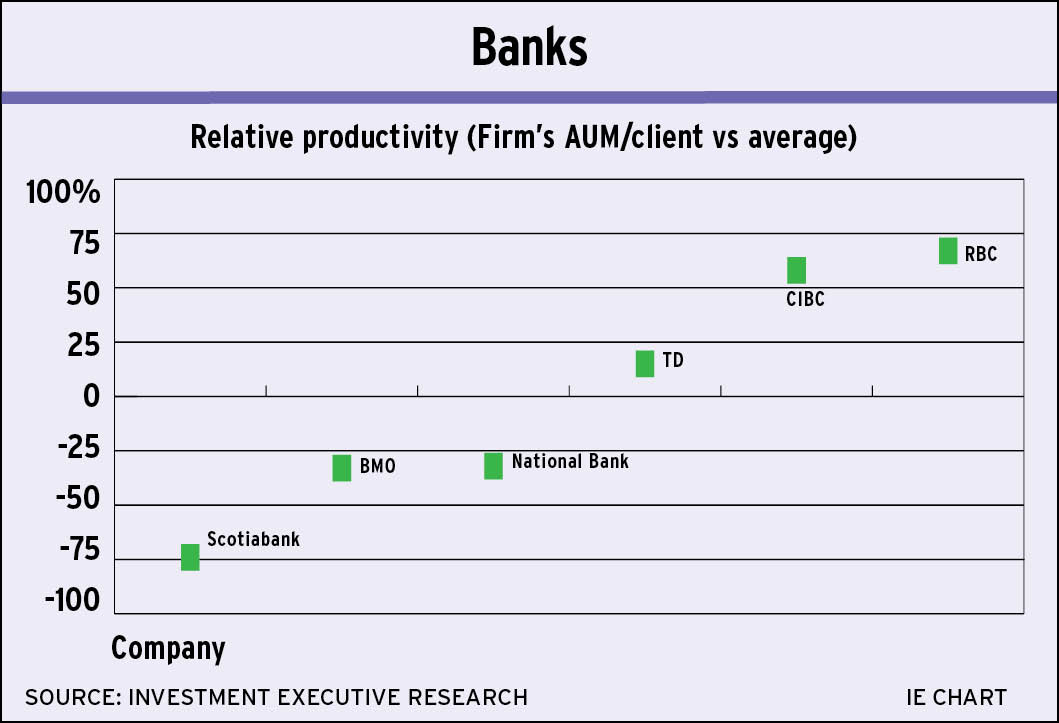

Banks

When it comes to the bank branch-based investment business, it’s clear Royal Bank of Canada and Canadian Imperial Bank of Commerce are the leaders in terms of relative average productivity. They both have average AUM/client that’s well ahead of the rest of the firms in this Report Card, with Toronto-Dominion Bank a somewhat distant third. The other banks are lagging, particularly Bank of Nova Scotia, which is well below the rest of the other firms in this channel.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive

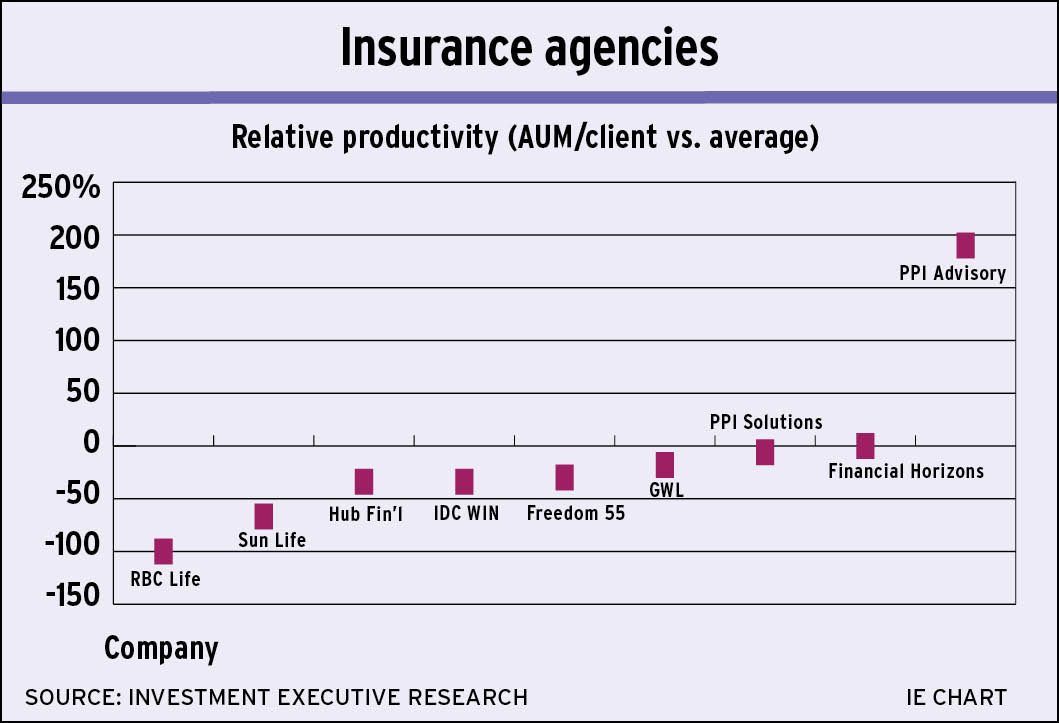

Gauging advisors’ relative productivity

Insurance agencies

Insurance remains an outlier among the various distribution channels when focusing on the investment side of the business, which is notably less important to the advisors in this space. The data show that most of this channel is clustered around the average, with PPI Advisory standing well apart from the others in terms of relative investment productivity.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive

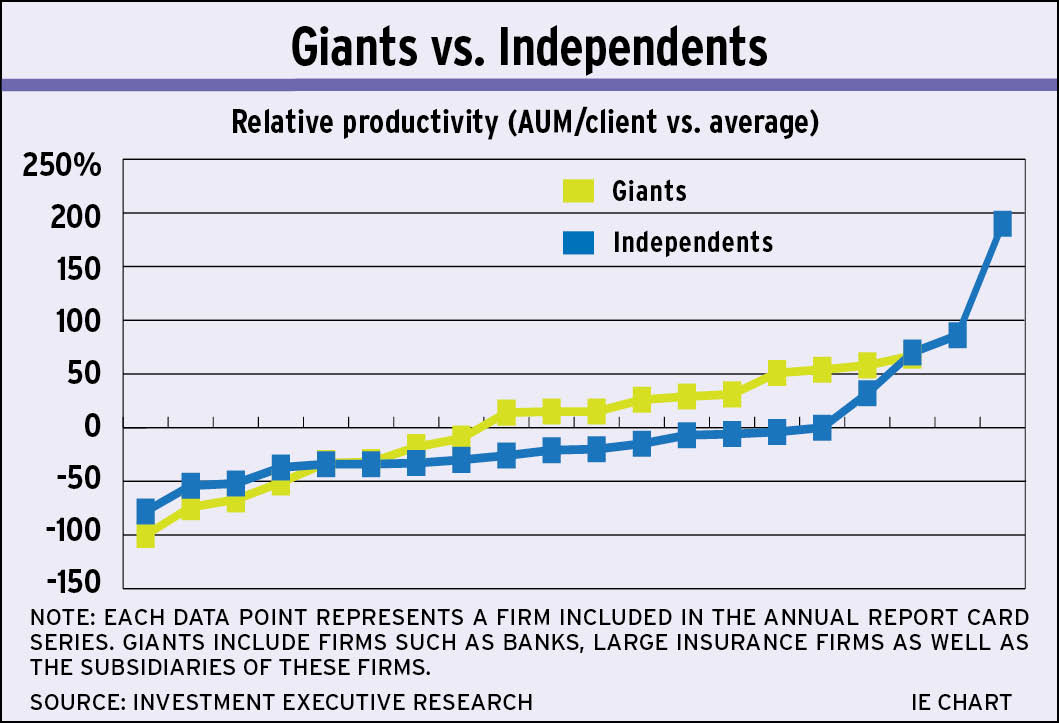

Gauging advisors’ relative productivity

Giants vs. independents

There’s a widely held belief that the Canadian financial services sector is dominated by a small group of huge players — the big banks and insurers — and IE’s data show that this does appear to be the case, at least in terms of relative productivity. Dividing the industry into “giants” (subsidiaries of the large banks and insurers, regardless of sector) and “independents” highlights the dominance of the big firms. Apart from a couple of independent outliers, advisors with the big players’ affiliates generally report higher relative productivity.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive

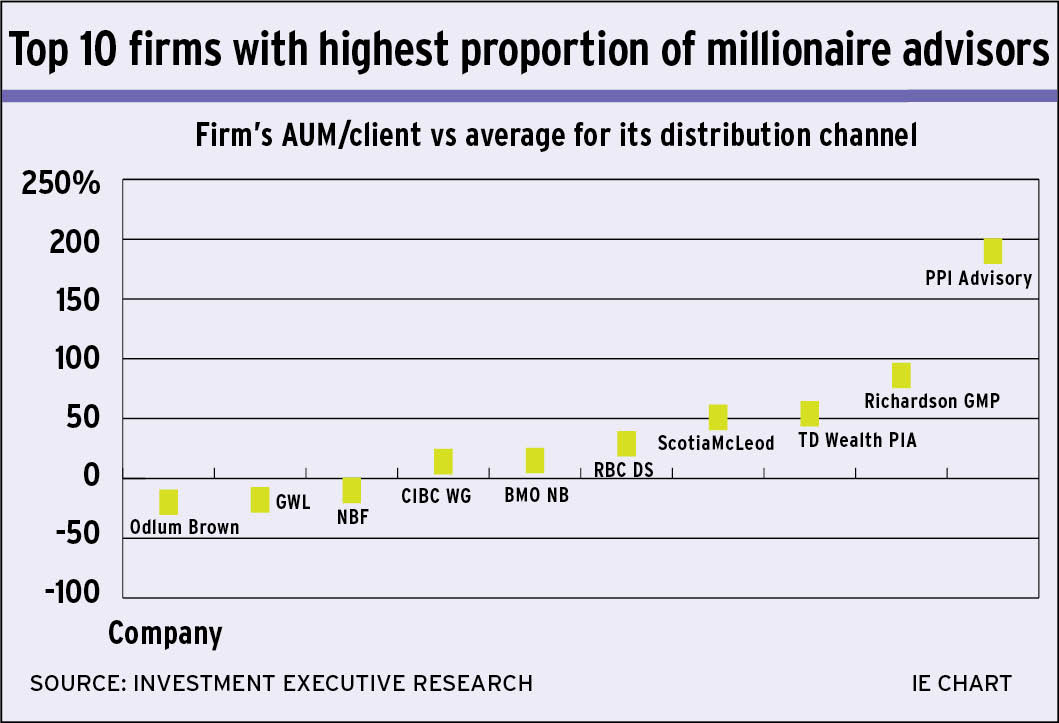

Gauging advisors’ relative productivity

Millionaires

Money may not be everything, but compensation is a likely a key motivator for many in the investment industry. This chart flags the top 10 firms in terms of proportion of advisors who report making at least $1 million a year. Interestingly, it shows that productivity isn’t everything. Some of the firms with a high proportion of highly paid advisors lag the industry in terms of average AUM/client.

Author: James Langton Source: Investment Executive Research Copyright: Investment Executive